Retirement Planning for Self-employed Individuals

Are you self-employed and dreaming of a worry-free retirement?

Planning for retirement is not only necessary for self-employed individuals; it is the absolute must-do. Excepting the employer-sponsored retirement plans, responsibility of securing a convenient future entirely depend on oneself. While this independence paves the way for flexibility, it also requires a proactive approach towards financial management. Here is the ultimate detailed guide that leads you through retirement planning specifically for the self-employed.

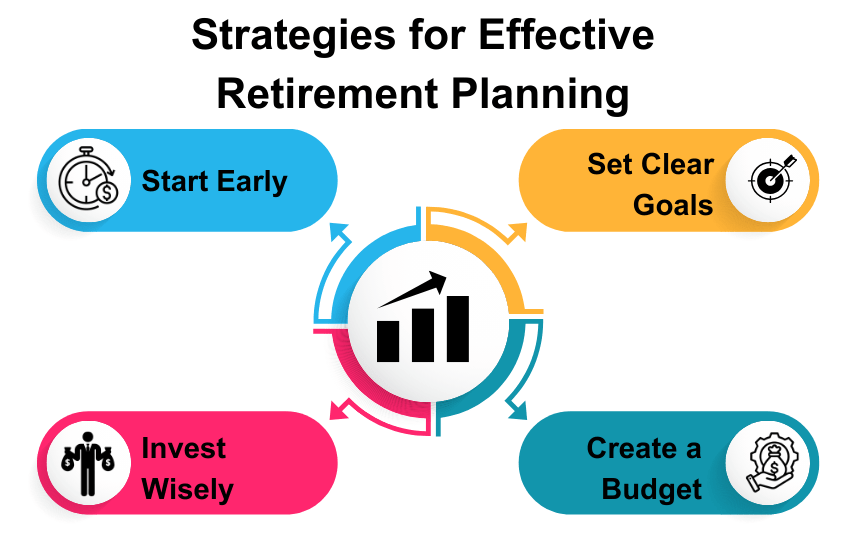

Strategies for Effective Retirement Planning

Start Early

The earlier you save, the better. Early deposits give your money time to grow and compound in your favor over the years. Even small amounts of money given early can create significant savings.

Set Clear Goals

Now define your perfect retirement: the age you want to retire, the lifestyle you wish to live, and the just amount of financial resource requirement. Well-defined aims will help to shape your saving and investing strategies so that everything stays on course.

Create a Budget

In fact, a good budget is needed to keep track of expenses and diversion of costs toward possible retirement savings. Identify areas where you can spend less and put that savings into your retirement plans.

Invest Wisely

You should consider working with a financial planner to create a diversified portfolio suited to retirement planning. You can save more in the long run and work to reduce risks if you hold a different type of asset in your portfolio. Select investment option which offers tax saving and help to maximize your assets portfolio.

Importance of Retirement Planning

As a self-employed individual, you are your own boss when it comes to retirement savings. You will not benefit from automatic employer contributions like conventional employees. You are responsible for developing and implementing retirement strategy and program. Following are a few important planned ways justifying why self-employed need planning for retirement:

Lack of Employer-Sponsored Plans

Since the company does not contribute anything to the retirement fund, it becomes necessary to draft a personalized retirement savings plan.

Irregular Income

Severe income fluctuations make it difficult to save on a very regular basis hence, a well-planned structure is vital for steady contributions towards retirement.

Potential for Higher Savings

A self-employed retirement plan typically allows larger contributions than a regular plan, thus making it possible to save even more.

Tax Benefits

Most retirement accounts for self-employed individuals have significant tax breaks, offering tax savings today as you save for future needs.

Business Succession Planning

For business owners, retirement planning invariably coincides with succession planning: making sure that the security and business transitions are financially supported.

Conclusion

Retirement planning for self-employed persons requires lots of hard work and proactive management. By being aware of your options, having clear goals, and making wise decisions, you can have a pretty good retirement plan to meet your needs when you age. Starting out or almost reaching retirement plan is never too late to take control over your financial future. Think about working with a financial advisor to help you customize a plan that is specific to your needs and goals.